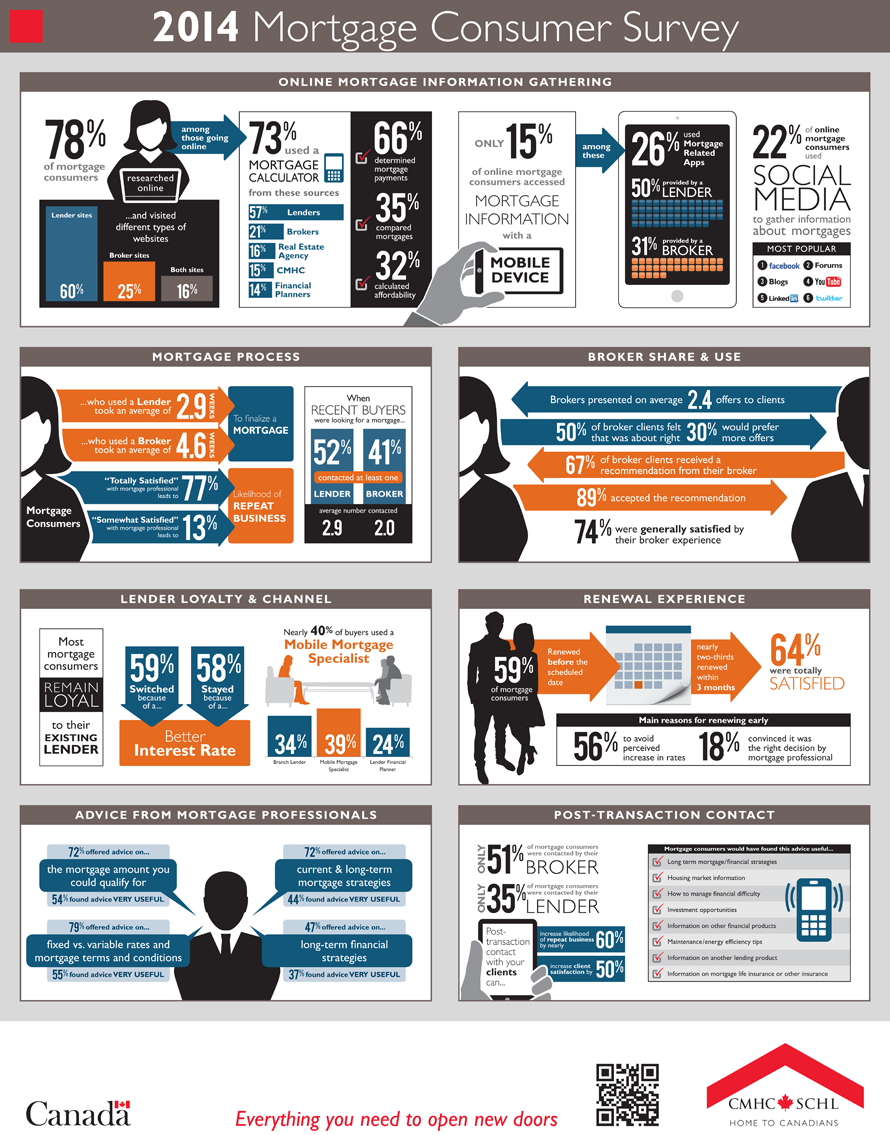

In March and April 2014, CMHC completed an online survey of 3,584 recent mortgage consumers, all prime household decision-makers who had undertaken a mortgage transaction in the past 12 months. Fifty-five percent had undergone a mortgage renewal, 22% had refinanced their mortgage, and 23% had purchased a home with mortgage financing. CMHC has conducted this survey since 1999. He are my thoughts using the Infographic and moving snakelike from the top left:

- I am glad to see many Canadians doing research online, not just following the ads they see on TV and hear on the radio

- I wish more would visit broker sites such as myself as I when I get questions from my clients, I know that could be a new blog post to hopefully answer questions that they might have. Also, I have produced many documents that might help give clients answers to questions they never have thought of. I think this is valuable.

- I like that Canadians are using mortgage calculators to try to work costs into their budget. I love doing these for my clients as I will do all the work and make the graphs and send them out and possibly add some more advice.

- I understand the 15% mobile device number. When I am making such a large purchase or making such big decisions, I like to sit in front of a larger computer to concentrate. With the increased of smart phones, I am sure this will go up. But getting $300k in financing is a whole lot different than buying a shirt from Banana Republic.

- I test out apps frequently, many of them mortgage related because I love seeing what is out there. Many are American based and miss out on CMHC information. Also they fail to include additional costs ie property taxes, condo/maintenance fees, bi-weekly payments or semi-annual compounding. I have yet to really find a perfect app. Maybe I should create it? On the plus side is Moreira Team website, which offers free, informative guides are for anyone wanting to learn more about the different home loan programs that are available.

- 22% used social media, that makes sense as social media should be used more towards engaging with people not dictating rates, etc. I welcome anyone to fire questions to me on twitter at @bachusky anytime or follow the #cmhTV hashtag for a weekly video podcast relating to the mortgage industry in Canada

- Brokers present at least 2.4 offers per client. I try to go for 2-4 with each, but based on great conversations with my client I can usually narrow down to 2-3 that would work in their specific situation. If 30% would like more, I will be giving more in the future. Only 74% were generally satisfied with their experience. That is way too low. Canadians deserve 100% satisfaction. I strive to get that every time.

- 41% of consumers going to a mortgage broker, although still very very low, is steadily increasing overall. I will continue to work towards promoting the use of mortgage brokers ahead of the banks as I used to work at two of the leading banks in the country and have seen the many problems that can arise from going to employees that do so much more than mortgages throughout a typical day. My career is solely towards mortgages, always reading and keeping up with the latest trends. As brokers, our lenders are frequently changing programs, rates and rules and for that we have to always be reading the daily emails and being in contact with the lenders. The lenders also take our advice and try to make things easier for the consumer.

- I like that consumers take about 2 weeks longer when deciding on the mortgage. It is an engaging process and just because you got a low rate with great conditions with lender A, doesn’t mean that during the time from approval to closing date that you can’t switch to company B if they offer something better. No additional documents or time needed on the consumer’s end. That is why I am in constant contact with my clients during this time. I want the savings to continually be increased for them. I want my clients to be completely satisfied and never feel pigeon-holed which they might feel at a bank. I know, I have been there before.

- I understand that most people feel loyal to their lender at time of renewal. However, I do feel that it would not be beneficial to not spend 2 minutes to email an agent like myself up to just get some professional advice that could potentially save you money. Sure, you might have to re-apply, but what is 2 hours of work to potentially save $1000s of dollars.

- I believe in always contacting your mortgage professional 120 days ahead of your renewal date as a precaution. Lenders will, however, do all they can to keep you with them. I see this as a good thing if you are completely satisfied with their administrative help and the rate they offer.

- Post-Transaction- wow, this is where Mortgage Professionals have to step up their game. I want to be involved with my clients from the first time they contact me and through their years. I feel with the hundreds of hours of studying, reading and being immersed in the financial industry I can give an outsider perspective to really help them. After a year, your clients might have had a raise, added more children, received inheritance, or many other material financial changes. For this, the payment and other options of the mortgage might not be the same as when you first received this. I will go over this with you and show you some graphs and best case scenarios annually.

- I go over all 4 of the options they give under “Advice from Mortgage Professionals”

Click the graphic below to see the Infographic in a full screen

CMHC’s 2014 Mortgage Consumer Infographic